Blockchain security cannot be explained without getting the basics right, so let's start with what exactly is blockchain!

What is Blockchain?

A blockchain is a continuously growing list of records, called blocks, which are linked and secured via cryptography. Each block has a reference to all the preceding blocks in a chain that's almost difficult to forge. All transactions within the blocks are double-checked and validated by a consensus mechanism, ensuring that each transaction is genuine.

Blockchain technology enables decentralization by allowing members of a decentralized network to participate. There is no single point of failure, and only one person may modify the transaction record at any moment. Blockchain technologies, on the other hand, have different levels of blockchain security.

What is Blockchain Security

Blockchain security is based on principles of cryptography, decentralization, and consensus, which guarantee trust in transactions. The data in most blockchains or distributed ledger technologies (DLT) is organized into blocks, with each block containing a transaction or group of transactions.

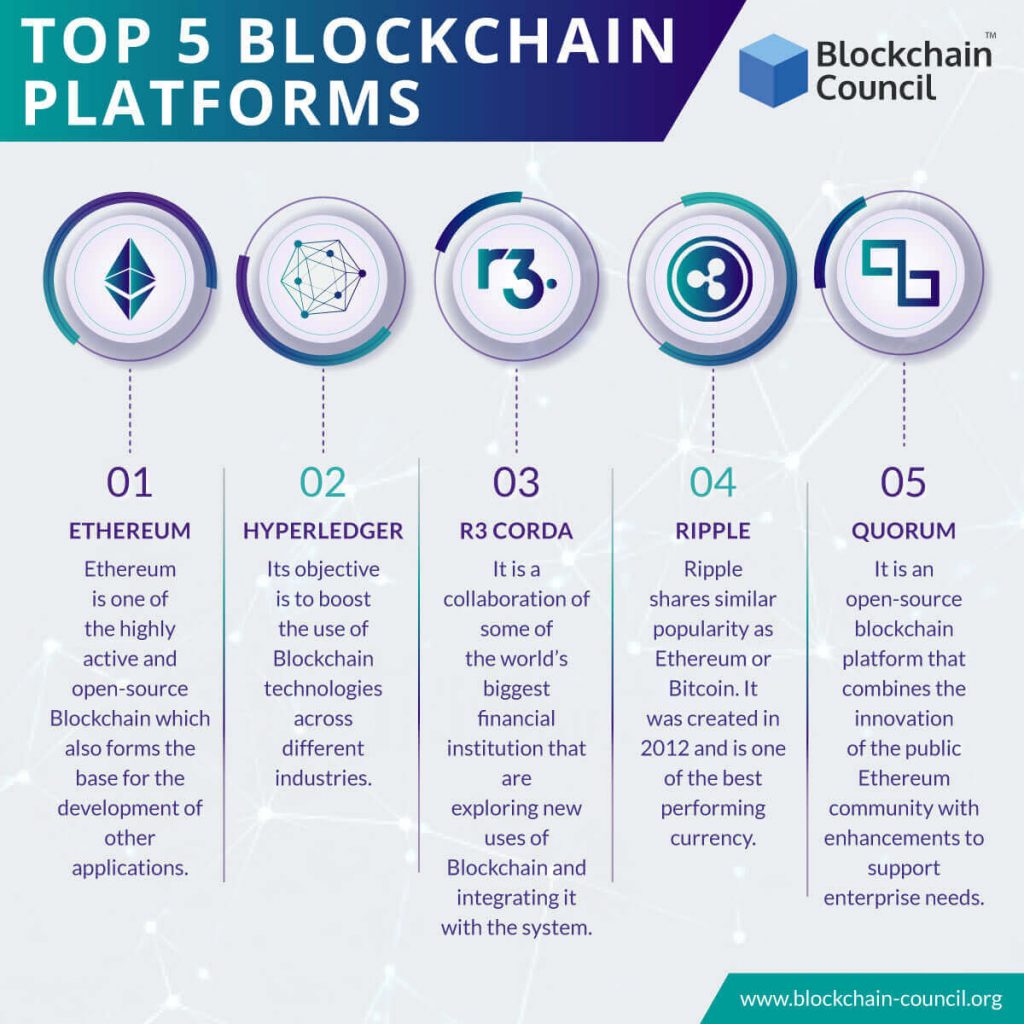

Blockchain Application Landscape: Top Blockchain Platforms

The blockchain, the technology on which the world's first cryptocurrency, "Bitcoin," was based, has changed the IT landscape in a way that has not been seen since the advent of the Internet.

The Financial Services sector has been the most proactive in utilizing Blockchain, however, there are a variety of Blockchain platforms now available that have cross-industry applications. The following are some industry leaders:

Ethereum

Ethereum is a public Blockchain platform that enables software developers to create decentralized applications on it and utilize the platform's cryptocurrency, "Ether," for financial transactions. Ether is the world's second most valuable cryptocurrency as of this writing.

Ripple

Ripple is a decentralized cryptocurrency that runs on the blockchain, and it's designed for cross-border financial transactions. The company employs a consensus mechanism that allows payments, exchanges, and remittances to occur in a dispersed manner using its cryptocurrency – XRP – which is currently the world's third-largest crypto.

Hyperledger

The Linux Foundation established Hyperledger in 2015, a collaborative, open-source platform for software developers to create diverse Blockchain platforms and frameworks to advance cross-industry Blockchain technologies.

The Hyperledger Fabric is one of the most well-known members of the Hyperledger family, which like other Blockchains maintains a distributed ledger, uses smart contracts, and enables participants to manage their transactions without boundaries.

However, Hyperledger Fabric is distinct from other Blockchains in many ways. While other Blockchains are open, permissionless systems that allow anybody to join the network (by requiring protocols like "Proof of Work" to validate transactions and secure the network), Hyperledger Fabric is instead a closed, permissioned system where participants must be pre-approved.

The Hyperledger Fabric is a private, "permissioned" Blockchain network that only requires its users to use a Membership Service Provider (MSP) to join.

The Difference in Security for Multiple Blockchain Types

Blockchain networks can have varying degrees of openness, depending on who is allowed to join and access data. Networks are generally classified as public or private, with the former determining who is permitted to participate and the latter describing how people gain access to the network.

Private and Public Blockchains

Anyone may join a public blockchain network, and participants are not required to identify themselves. A public blockchain uses internet-connected computers to validate transactions and reach agreements. Bitcoin is perhaps the most well-known example of a public blockchain, with "bitcoin mining" as its method of consensus creation.

Miners on the bitcoin network attempt to solve a difficult cryptographic issue in order to generate proof of work and hence validate the transaction. Outside of public keys, this sort of network has few identities and access controls.

Public blockchains, on the other hand, allow anybody to join and participate — but only known firms may do so. A private, members-only "business network" is made up of these organizations.

In a permissioned network, a selective endorsement is used to reach a consensus. Only users with special access and permissions can maintain the transaction ledger. This sort of network necessitates more stringent security measures.

When developing a blockchain application, it's important to determine which type of network will best meet your company's objectives. Private and permissioned networks may be tightly controlled, making them more suitable for regulatory and compliance reasons. Public and permissionless networks, however, can achieve greater decentralization and distribution.

- Private blockchains are limited and typically exist within businesses. Membership is controlled by a single entity or consortium.

- Public blockchains, on the other hand, are available to everyone who wishes to participate and audit transactions.

- Permissioned blockchains are restricted to a small number of users who have been given identities using certificates.

- There are no limits on processors for permissionless blockchains.

Top Blockchain Security Attacks, Hacks and Issues

Blockchain technology, like other technologies before it, is not exempt from cyberattacks and fraud. Those with malevolent intent can use known flaws in blockchain infrastructure to their advantage, and they have in the past. Here are a few examples:

Stolen Keys

The theft of approximately USD 73 million in bitcoin from one of the world's major cryptocurrency exchanges, Hong Kong-based Bitfinex, revealed that the currency is still a significant risk. The stolen private keys were most likely responsible for the breach.

Code exploitation

The DAO (Decentralized Autonomous Organization), a cryptocurrency venture capital fund run through blockchain technology similar to Bitcoin, was robbed of more than $60 million worth of ether digital currency — about a third of its value — due to code exploitation.

Hacked Computer

In July 2018, Bithumb, one of the world's largest Ethereum and bitcoin cryptocurrency exchanges was hacked. The intruders obtained 30,000 people's data and stole approximately $870,000 in bitcoin. Despite the fact that it was a computer belonging to an employee - not the core servers - this incident prompted concerns about overall security.

Understanding How Blockchain Attacks Happen

Hackers and fraudsters employ four primary strategies to threaten blockchains: phishing, routing, Sybil attacks, and majority assaults.

Routing attacks

Hackers can tamper with data as it travels to internet service providers. Data may be intercepted as it goes from one entity to the next. Blockchain participants are generally unable to detect an attack, thus everything appears normal. Fraudsters, on the other hand, have gained access to sensitive information or currency.

Sybil attack

In a Sybil attack, hackers create and utilize a large number of false network identities to overwhelm the network and bring down the system. The Book character diagnosed with a multiple identity disorder is known as Sybil.

Phishing attacks

A phishing scam is when a hacker attempts to get access to a user's credentials. Fraudsters send emails to wallet key holders that appear to be from a genuine source, attempting to acquire their information. The emails appear to be from Google or Facebook and ask for login information via phony links. Having access to a user's credentials and other critical data might result in both the user and the blockchain network being harmed.

51% attack

Mining requires a significant amount of computational power, particularly for public blockchains with millions of users. However, if a miner or a group of miners can accumulate enough resources, they could obtain more than 50% of the mining power in a blockchain network. Having more than half of the power means having control over the ledger and the ability to influence it. However, A 51% attack is not possible on private blockchains.

Blockchain Security for the Enterprise

It's critical to think about security at all levels of the technology stack while developing an enterprise blockchain application, as well as network governance and permissions. Using both traditional security controls and technology-specific ones is essential for a complete security strategy for an enterprise blockchain solution. The following are some of the security safeguards unique to enterprise blockchain solutions:

- Identity and access management

- Key management

- Data privacy

- Secure communication

- Smart contract security

- Transaction endorsement

Look for a platform that allows you to design a legal and safe system while also assisting you in meeting your company objectives. Look for a suitable production-grade platform for developing blockchain solutions that may be deployed in the technology environment of your choosing, whether on-premises or with your preferred cloud vendor.

Blockchain Security Tips and Best Practices

Before concluding our article, let's take a look at some blockchain security tips & best practices:

- When creating a private blockchain, make sure it's set up in a safe and resilient infrastructure.

- Poor business technology choices and procedures can lead to data security issues as a result of their flaws.

- Take into account commercial and governance risks.

Financial consequences, reputation concerns, and compliance issues are all examples of business risks. Blockchain technology's decentralized nature poses significant governance risks, which need tight controls on decision criteria, governing rules, identity and access management.

Blockchain security is all about managing the risks of a blockchain network. A blockchain security model is formed as a result of this decision. To ensure that your blockchain solution is adequately secured, create a blockchain security model.

Administrators must create a risk model that can account for all existing, potential, and prospective risks when they implement a blockchain solution security model.

Administrators must then assess the threats to the blockchain solution and develop a threat model. Finally, administrators must establish the security measures that reduce the dangers and threats based on the following three categories:

- Enforce security controls that are unique to blockchain

- Apply conventional security controls

- Enforce business controls for blockchain

Taking Blockchain's security for granted may be a mistake, as it is one of the most secure data protection solutions available today. With time, Blockchain technology will continue to evolve, and its vulnerabilities will emerge. It's only a matter of time until hackers figure out how to break into Blockchain networks.

It's critical to secure your Blockchain from the start by using strong authentication and encryption key vaulting techniques.

Leave a Reply